How Sizing Solutions Sync Perfectly With Buy Now, Pay Later Plans

Buy Now, Pay Later has shifted from a generally accepted alternative to traditional credit to a somewhat polarizing issue within the eCommerce apparel industry. Proponents of BNPL claim that the service offers crucial financial assistance to those who otherwise would go without it while also providing flexible (and often, interest-free) payment plans to shoppers across all income brackets. Detractors cite the noticeable rises in shopper conversion rates as a sign that BNPL encourages overconsumption and overall financial recklessness.

As apparel brands scramble to construct their Q4 eCommerce stack in preparation for the peak shopping season, the question on everyone's mind is whether BNPL is a proper complement to their on-site experience. Will your more price-sensitive shoppers rely on BNPL to navigate these tough economic times? How can your brand reduce or eliminate the drawbacks associated with the service? All of these questions and more will be addressed in the article below.

Let's take a deeper look into BNPL phenomenon, and how the synergies between these plans and modern sizing solutions can result in a significant net positive for your eCommerce apparel brand.

How Buy Now, Pay Later Plans "Actually" Work

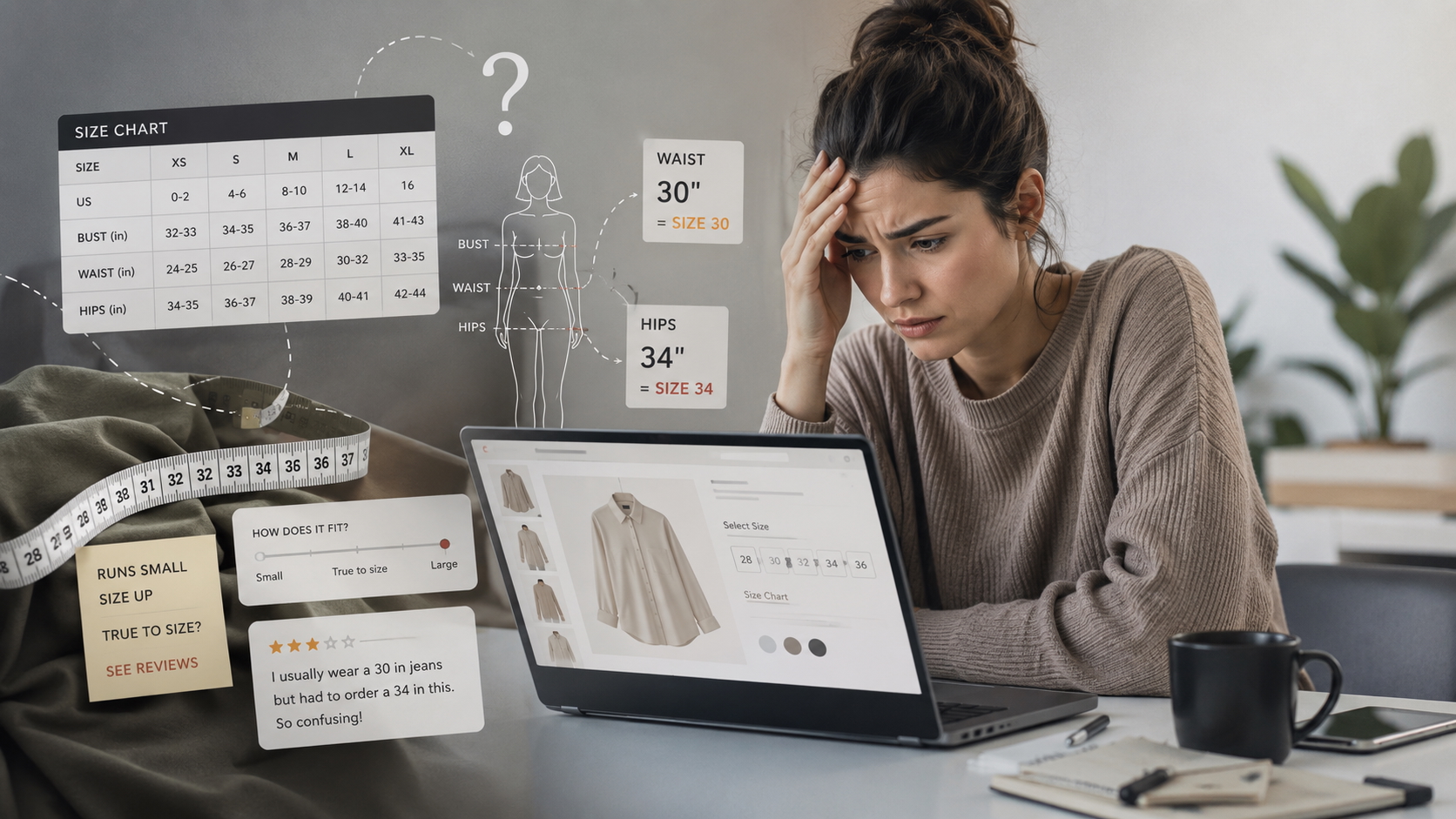

-min%201.png)

For those unfamiliar with Buy Now, Pay Later plans, let's briefly discuss how they actually work.

When a shopper arrives at a checkout page, they are faced with the option to pay for the product in full using traditional methods (credit/debit card) or pay in several installments through a BNPL provider such as Affirm or Klarna.

If the shopper opts to go the BNPL route, they'll enter several unique details about themselves(street address, SSN, etc.) so that the BNPL provider can run a soft credit check to determine the shopper's creditworthiness. Because this is a soft credit check, it is not reported to credit bureaus and cannot affect the shopper's credit score like a hard credit check would.

If the shopper is approved, the provider will take a cut of the sale (usually 2-8%), and the shopper's payment plan begins. Simple right? Well, that's just the tip of the iceberg. Now that the transaction has been completed, the post-purchase journey begins.

While most BNPL providers offer no-interest payment plans, they are bound by relatively short time windows. For example, shoppers are often given eight weeks to pay off their debt, usually making one payment every two weeks for a total of four payments. While this is perfectly in line with most shoppers' bi-weekly cash flow, if any of the payments are late, there are additional fees the shopper must pay on top of the initial balance.

Why BNPL Plans Are Trending in 2022

With the noticeable shift in shopper preference toward eCommerce (driven by the pandemic), BNPL is currently one of the most prominent trends in the industry. According to SimilarWeb, fashion and apparel are the fastest-growing shopping categories for BNPL platforms, with a 24% increase in traffic share in 2021 alone.

But BNPL's rise to prominence isn't only due to shifting shopper purchasing preferences. As economic headwinds persist, inflation-stricken shoppers looking to complete their holiday shopping lists will find it difficult to finance these purchases without the assistance of alternative payment plans.

The severity of the current economic climate is further highlighted by BNPL's recent uptick in use for non-discretionary goods like gas and groceries. As clothing becomes somewhat of a lesser priority with shoppers across all income brackets, your brand will need to be nimble in its approach to alternative payment plans in Q4.

The Double-Edged Nature of BNPL Plans

There's an interesting dichotomy between the benefits and drawbacks of Buy Now, Pay Later plans. For example:

Conversion rates - Brands offering BNPL plans see a 20-30% average increase in conversion rates vs. those not offering the service. While these look like great numbers on the surface, potential overconsumption can harm the shopper, your brand, and the environment through excessive shipping emissions and textile waste.

AOV - Affirm and Klarna have reported as high as an 85% lift in average order value from brands using their services. This substantial rise in AOV is primarily due to shoppers having to pay little to nothing upfront, making the purchases seem more benign than they truly are during checkout.

Returns Processing - Relying on a third party to fulfill online transactions might give shoppers more financial freedom, but returns through BNPL plans can be much trickier to process than run-of-the-mill online returns. In most cases, the shopper will need to reach out to the brand and the BNPL provider for a full refund and will be required to fulfill their scheduled payments on time while the return is being processed. In addition, any interest paid during this period is often non-refundable.

Capitalizing on the Benefits of BNPL

With the key pitfalls currently surrounding BNPL being potential overconsumption and returns processing, providing your shoppers with enhanced clarity on sizing and fit can significantly remedy these issues.

While eCommerce sizing tools may appear unrelated to BNPL plans, hear us out. The underlying issues behind bracketing and other defensive purchasing habits are sizing, fit, and accurate product representation. When your shoppers are faced with outdated and inconsistent size charts or model dimensions from people who look nothing like themselves during the most critical step of their journey, their urge to purchase multiple sizes and return what doesn't fit increases exponentially.

This is where eCommerce sizing tools like WAIR come into play. Not only do these solutions curb overconsumption by providing your shoppers with personalized and accurate size recommendations, but they also help reduce the likelihood of returns by eliminating size confusion from the shopper's journey.

A great example of a synergistic blend of BNPL and modern sizing solutions is WAIR and Try Now Buy Later (TryNow). TryNow is a BNPL service, but with a twist. They enable shoppers to order apparel products without paying for them until one week after the product has arrived, allowing the shopper to make true first-hand impressions of the product itself. Because the shopper only pays for what they keep, they can convert with confidence knowing they will not be penalized for choosing the wrong size or style.

While TryNow's solution can significantly boost shopper confidence, the last thing brands want to see is a potential influx of returns through size sampling. With WAIR's seamless and personalized size recommendations, the chances of size sampling are reduced exponentially, enabling brands to enhance the user experience with BNPL without the corresponding drawbacks associated with the services.

Effectively Partnering With BNPL Providers is Key

Regardless of the industry's stance on BNPL, these services have somewhat cemented themselves within the world of apparel eCommerce and (for the time being) aren't going anywhere. Learning how to effectively pair sizing solutions with BNPL to reduce shopper friction and improve the user experience can be a significant boon to any growing (or established) eCommerce site, especially during the Q4 peak shopping season.

Interested in learning more about WAIR? Schedule a demo here, and be sure to follow us on Twitter, Instagram, LinkedIn, and Facebook for all your fashion content needs!

Want to be notified of our newest episodes?

Subscribe to our Podcast!